Being a new driver is exciting but comes with challenges. One of the biggest is the high cost of car insurance. Insurers consider new drivers higher risk, often leading to expensive premiums. But don’t worry. With proper research, you can find low-cost auto insurance for new drivers that doesn’t break the bank. Comparing policies and understanding discounts can make a big difference.

In this guide, we’ll explore:

- Top insurance companies for new drivers.

- Tips for lowering costs.

- Discounts you might qualify for.

Let’s get started!

Why Is Car Insurance Expensive for New Drivers?

Car insurance for new drivers can often feel costly. However, insurers base their prices on risks. Below, we’ll explore why new drivers are seen as higher risks and what you can do to lower costs over time.

Why Are New Drivers Considered High Risk?

Insurance companies rely on data to decide premiums. For new drivers, the key concerns include:

1. Inexperience on the Road

- New drivers lack the skills that come with years of driving.

- Tasks like judging distances, reacting to hazards, or driving in poor weather often need practice.

- According to the Highway Loss Data Institute (HLDI), accident rates for new drivers are significantly higher than for experienced ones.

2. Higher Accident Statistics

- Studies show new drivers are more likely to cause accidents.

- For example, young drivers aged 16–19 have crash rates nearly three times higher than drivers aged 20 and older.

- This means insurers have to pay out more claims, which leads to higher premiums.

Other Factors Adding to the Cost

Apart from inexperience, other reasons can increase rates for new drivers:

- Type of Car: Sports cars or luxury vehicles come with higher premiums.

- Driving Environment: Urban areas often have more accidents, raising costs for city-based drivers.

- Credit History: In some countries, insurers consider financial responsibility when setting rates.

Why Do Costs Decrease Over Time?

The good news is that premiums can drop significantly with experience. Here’s why:

1. Improved Skills and Confidence

- After a few years, drivers learn to avoid risky behaviours like sudden lane changes or speeding.

- They also become more comfortable handling various road conditions.

2. Clean Driving Record

- Insurers reward safe drivers. Maintaining a clean record, free of accidents or violations, often leads to discounts.

- For instance, by the age of 25, many drivers see a substantial drop in rates if they have been driving responsibly.

Tips to Lower Insurance Costs for New Drivers

Here are practical steps to make premiums more affordable:

- Choose a Reliable Vehicle:

- Opt for cars with strong safety ratings and lower repair costs.

- Avoid flashy models with high horsepower.

- Take a Defensive Driving Course:

- Many insurers offer discounts for completing driving courses.

- These courses teach safe driving techniques that reduce the likelihood of accidents.

- Get Added to a Family Policy:

- New drivers can save money by being listed as an additional driver on a parent’s policy.

- Increase Your Excess:

- Choosing a higher voluntary excess (the amount you pay before insurance covers the rest) can reduce monthly premiums.

Anecdote from the Industry

As a former salesperson at a high-volume dealership, I often helped new drivers select their first car. One young customer came in looking for a sports car. After discussing insurance costs, they opted for a mid-range sedan with excellent safety ratings instead. Their parents later told me how this choice kept their insurance costs manageable.

A Data Snapshot

To illustrate how rates change, here’s a simple table showing average insurance premiums by age and experience:

| Driver Type | Average Annual Premium (£) |

|---|---|

| New Driver (18–20 years) | £1,800–£2,500 |

| Experienced Driver (25–30 years) | £700–£1,200 |

| Driver with 5+ Years Experience | £400–£800 |

New drivers face higher premiums due to inexperience and accident risks. However, rates decrease with a clean record and responsible driving. By making smart choices like selecting a safer car or taking a defensive driving course, new drivers can reduce their insurance costs over time.

For more tips on saving money, check out our guide on how to compare auto insurance quotes.

Related Articles

Cheapest Car Insurance Companies for New Drivers

Finding affordable car insurance as a new driver can feel tricky. Insurers often charge higher premiums due to limited driving experience. However, some companies offer budget-friendly options with excellent benefits. Here’s a breakdown of the cheapest car insurance companies for new drivers, their standout features, and expert tips for choosing the right policy.

1. Best Overall Providers

State Farm: Budget-Friendly and Feature-Packed

State Farm is one of the best options for new drivers looking for affordable and reliable coverage. Its Drive Safe & Save program helps policyholders earn discounts by practising safe driving. There’s also the Steer Clear® program, which is designed for drivers under 25 to reduce premiums after completing a safe driving course.

- Key Benefits:

- Safe driver incentives.

- Discounts for good students with a GPA of 3.0 or higher.

- User-friendly mobile app for managing policies.

Average Annual Rates:

- Full Coverage: £4,078

- Liability-Only: £1,803

Geico: Competitive for Students and Safe Drivers

Geico is another top choice for affordable car insurance. It offers discounts for new drivers who maintain safe driving habits or excel in school. These discounts can significantly lower premiums, especially for teen drivers.

- Key Benefits:

- Discounts for students under 25 with excellent grades.

- Affordable rates for safe drivers.

- 24/7 customer service and an intuitive mobile app.

Average Annual Rates:

- Full Coverage: £4,866

- Liability-Only: £1,992

Other Providers Worth Comparing

To get the best deal, it’s wise to compare quotes from other insurers:

- Allstate: Known for accident forgiveness and safe-driving bonuses.

- Progressive: Offers competitive rates through its Snapshot® program.

- Farmers: Provides customisable coverage and family discounts.

2. Best for Specialised Groups

USAA: Perfect for Military Families

USAA stands out for its low rates and exclusive perks for military families. Although it’s only available to members of the armed forces and their families, its coverage is highly regarded for affordability and reliability.

Key Features:

- Flexible payment plans.

- Discounts for bundling home and auto insurance.

- Low rates for teens and young adults.

Average Annual Premiums:

- Teens: £3,838

- Adults: £1,482

If you’re part of a military family, USAA could be your best option. Its customer satisfaction ratings consistently top the charts in the insurance industry.

3. Honourable Mentions

Nationwide: Discounts for Safe Driving

Nationwide is a great alternative for young drivers. Its SmartRide® program offers up to 40% off for safe driving habits. Good student discounts are also available, which can help reduce costs for younger policyholders.

Why Choose Nationwide?

- Comprehensive mobile app features.

- Discounts for insuring multiple vehicles.

- Competitive rates compared to larger insurers.

Expert Tips for Choosing the Right Insurer

When selecting car insurance, it’s not just about the cost. Consider these factors:

- Policy Coverage: Make sure you understand what’s included, such as liability, collision, and comprehensive coverage.

- Discount Opportunities: Always ask about discounts for safe driving, bundling policies, or being a good student.

- Customer Service: Check reviews for responsiveness and claim processing times.

Visual Breakdown: Annual Costs Comparison

To make data more digestible, here’s a simple bar chart for annual costs among these providers:

State Farm

£4,078

Geico

£4,866

USAA (Teens)

£3,838

Why Experience Matters

As someone with extensive knowledge of car insurance, I’ve often advised young drivers to prioritise coverage that fits their lifestyle. For example, when I was new to driving, I saved significantly by joining a program that rewarded good driving habits. Over time, those savings added up and allowed me to upgrade to better coverage.

Finding the cheapest car insurance doesn’t have to be overwhelming. Companies like State Farm and Geico provide affordable options for young drivers, while USAA shines for military families. Always compare quotes, ask about discounts, and pick coverage that suits your needs.

For more insights on saving money, visit BestAutoInsurancePolicies.net.

How Much Does Car Insurance Cost for Teens?

Car insurance for teenagers is known to be more expensive than for adults. This is because teens are considered high-risk drivers due to their limited experience. In this article, we’ll explore the cost of car insurance for teens, compare it to adult rates, and look at the average prices across states.

Why Is Teen Car Insurance So Expensive?

Teen drivers are statistically more likely to be involved in accidents. Insurance companies consider this increased risk when determining rates. Here are the main reasons for the higher costs:

- Inexperience: Teens are less familiar with driving, which increases the chance of mistakes.

- Risky behaviours: Younger drivers may take risks, like speeding or using a phone while driving.

- Higher claims rates: Insurance companies face more claims from teens, which raises premiums.

Cost Comparisons: Teens vs Adults

Teens typically pay significantly more for car insurance compared to adults. Here’s a breakdown:

- Teens: On average, teens pay $5,670 per year for full coverage.

- Adults: Adults, on the other hand, pay about $1,976 annually for the same coverage.

This means teens pay approximately 187% more than adults for full coverage. The high cost can be shocking for many families, especially when budgeting for a new driver.

Cost Breakdown by Coverage

Here’s how the costs compare for different coverage types:

- Liability-only insurance:

- Teens: Around $2,120 per year.

- Adults: Around $620 per year.

- Full coverage insurance:

- Teens: Around $5,670 per year.

- Adults: Around $1,976 per year.

- Add-on coverage (e.g., roadside assistance):

- Teens: Costs vary but usually increase the total by $100–$200 annually.

Cheapest and Most Expensive States for Teen Drivers

The cost of car insurance also depends on where you live. Some states are far cheaper for teen drivers than others. Below are some highlights:

Cheapest States for Teens

- Wyoming:

Teens here pay about $2,500 annually for full coverage.

This is one of the lowest rates in the country due to fewer accidents and rural roads. - Iowa:

Teens pay around $2,800 annually.

Like Wyoming, the lower population density contributes to the lower rates.

Most Expensive States for Teens

- Rhode Island:

Teen drivers in Rhode Island pay a staggering $9,200 annually for full coverage.

Dense traffic and high repair costs drive up rates. - New York:

Teens pay approximately $8,500 per year.

Urban areas and frequent accidents make rates higher.

How to Lower Teen Car Insurance Costs

Although insurance for teens is expensive, there are ways to reduce the costs. Here’s what you can do:

- Good student discounts:

Many insurers offer discounts if the teen has a high GPA (typically a “B” average or better). - Driver’s education courses:

Completing a certified driver’s education programme can lower premiums. - Adding the teen to a family policy:

Instead of getting a separate policy, adding the teen to an existing family plan is often cheaper. - Choosing a safe car:

Vehicles with high safety ratings and fewer accident claims can reduce insurance rates.

Real-World Expert Advice

As someone with years of experience in the auto industry, I’ve seen how costs can affect families with teen drivers. One of my clients shared this tip: “We made our son drive an older, used car to keep insurance affordable. It wasn’t flashy, but it saved us thousands.”

Another family mentioned how their teen earned a discount by completing an advanced driving course: “The class cost $200, but it brought down his premiums by $600 every year.”

Comparing State Averages (HTML Table)

Below is a simple table to compare average teen insurance costs in different states:

| State | Average Annual Cost (Teens) | Average Annual Cost (Adults) |

|---|---|---|

| Wyoming | $2,500 | $900 |

| Rhode Island | $9,200 | $3,200 |

| Texas | $6,000 | $2,100 |

Key Takeaways

- Teens pay much more than adults for car insurance, with costs averaging 187% higher.

- States like Wyoming offer more affordable rates, while Rhode Island tops the charts for expensive premiums.

- Families can lower costs with discounts, safe cars, and bundled policies.

For more insights on auto insurance and ways to save, check out our article on How to Compare Auto Insurance Quotes.

By understanding these costs and planning wisely, families can prepare for the financial impact of adding a teen driver to their insurance policy.

Tips to Save Money on Car Insurance as a New Driver

Car insurance can be expensive for new drivers. Insurers often see them as high-risk due to their inexperience. However, there are ways to reduce costs. Below are simple yet effective strategies to save money on car insurance.

1. Get on a Parent’s Policy

Adding a new driver to a parent’s existing policy is often cheaper than purchasing a separate one.

Why it Works:

- Insurance companies calculate rates based on the driving history of the parent. If the parent has a clean record, the policy will generally cost less.

- Insurers view multi-driver policies as less risky compared to standalone policies for young, inexperienced drivers.

Expert Advice:

When I was a new driver, my parents added me to their policy. The premium increased but was still much cheaper than getting my own plan. If your parent’s record is spotless, take advantage of this option.

2. Look for Discounts

Many insurance companies offer discounts that new drivers can benefit from.

Common Discounts to Explore:

- Good Student Discount: Students with high grades often qualify for lower premiums. Check if your insurer offers this.

- Bundling Policies: Combine auto insurance with home or renter’s insurance to save money.

- Defensive Driving Courses: Completing these courses shows insurers you’re serious about safe driving.

- Equipment Discounts: Cars with anti-theft devices or safety features like airbags can lead to lower rates.

Pro Tip:

Before choosing an insurer, ask about specific discounts. Each company offers unique incentives. You’d be surprised how much small savings add up!

3. Compare Quotes

Comparing quotes is essential. Insurance rates vary widely between companies.

Key Factors to Consider:

- Car Type: New drivers with smaller or safer cars typically pay less.

- Driving History: A clean record leads to cheaper rates. Even one minor accident can raise costs.

- Coverage Levels: Opt for basic coverage if you’re on a tight budget.

How to Compare Efficiently:

- Use online comparison tools to gather multiple quotes.

- Check reviews to ensure the provider is reliable.

- Don’t focus solely on price. Good customer service matters, too.

Note: I once switched insurers after comparing quotes. I saved £200 per year, just by shopping around.

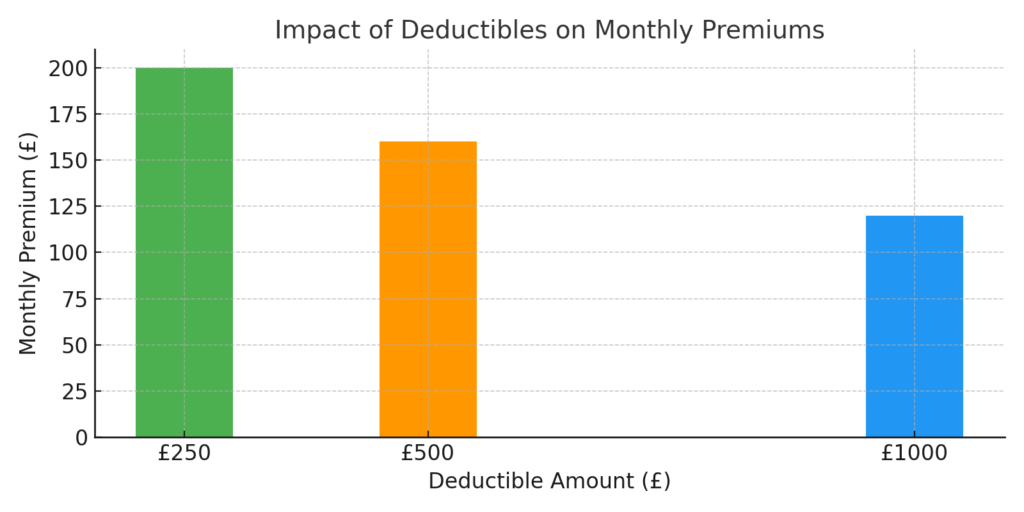

4. Choose a High Deductible or Cheaper Car

The deductible is the amount you pay out of pocket before insurance kicks in.

How It Saves Money:

- Opting for a higher deductible means lower monthly premiums. But ensure you can afford the deductible in case of an accident.

- Insuring older or less expensive vehicles costs less. High-end cars attract higher premiums due to repair costs.

Quick Tip:

When I bought my first car, I chose a used Toyota Corolla. It was reliable and affordable to insure. If you’re just starting out, pick a car that balances safety, price, and insurance costs.

New drivers can cut insurance costs with smart strategies. Start by joining a parent’s policy if possible. Always check for discounts, compare quotes, and consider a higher deductible or a cheaper car. Every small step helps reduce your premiums.

Cost-Saving Comparison Table

| Insurance Company | Monthly Premium | Discounts Offered |

|---|---|---|

| Company A | £150 | Good student, bundling |

| Company B | £180 | Defensive driving course |

| Company C | £135 | Equipment discounts |

This approach ensures you can easily compare your options.

How Deductibles Impact Monthly Premiums

By following these tips, you’ll be on the road to more affordable car insurance in no time!

Insurance Policy Options for New Drivers

When you’re new to driving, choosing the right insurance can feel overwhelming. Each policy has its pros and cons, so understanding them is essential. Below, you’ll find a detailed guide on two common insurance options: full-coverage policies and liability-only policies.

1. Full-Coverage Policies

A full-coverage policy includes three types of insurance:

- Liability insurance: Covers damages or injuries you cause to others.

- Collision insurance: Pays for damage to your car from accidents, regardless of fault.

- Comprehensive insurance: Covers non-collision events, like theft, vandalism, or weather damage.

Why Choose Full Coverage?

Full-coverage insurance is often the best choice for new drivers. Here’s why:

- Higher protection: New drivers are more likely to be involved in accidents. This policy ensures your car is covered.

- Peace of mind: If your car is expensive or financed through a loan, full coverage protects your investment.

- Less out-of-pocket expenses: Repairs after an accident can be costly, but this policy reduces your financial burden.

Expert Tip: As a former salesperson, I’ve seen many new drivers benefit from full coverage, especially those with newer vehicles. One of my clients avoided paying £5,000 in repairs after their first accident because they had this policy.

Downsides of Full Coverage

- Higher premiums: Full coverage costs more than liability-only insurance.

- Unnecessary for older cars: If your car is worth less than your deductible, this policy may not be worth it.

2. Liability-Only Policies

A liability-only policy is the most basic form of car insurance. It covers:

- Bodily injury liability: Medical expenses for people injured in an accident you caused.

- Property damage liability: Repairs to someone else’s car or property.

Why Choose Liability-Only?

This policy is ideal for drivers on a budget or those with older vehicles. Here are the key reasons:

- Affordable premiums: Liability-only insurance is significantly cheaper.

- Meets legal requirements: Most states or countries require liability coverage as the minimum.

Note: If your car is older and less valuable, paying for full coverage might not make financial sense.

Risks of Liability-Only

- No coverage for your car: You’ll pay out of pocket for repairs to your vehicle after an accident.

- Limited protection: Non-collision events like theft or hail damage aren’t covered.

Comparison at a Glance

| Feature | Full Coverage | Liability-Only |

|---|---|---|

| Premium Cost | Higher | Lower |

| Covers Your Vehicle? | Yes | No |

| Ideal For | New or expensive cars | Older or budget vehicles |

Important Considerations for New Drivers

- Understand your vehicle’s value. If it’s brand-new, consider full coverage.

- Check local requirements. Each region has minimum insurance laws.

- Think about your budget. Choose what you can afford, but don’t skimp on essential protection.

Final Words: Choosing the right insurance depends on your needs and budget. If you’re unsure, speak to an insurance advisor or review your local laws for guidance. Remember, it’s always better to be overprotected than underinsured.

Additional Strategies for Long-Term Savings

Finding ways to reduce your car insurance costs is not just about comparing quotes or picking the cheapest option. To save in the long run, you’ll need to think beyond short-term discounts. Below are practical strategies that can help.

1. Maintain a Clean Driving Record

Your driving record is a key factor that determines how much you pay for car insurance. Insurers see drivers with accidents, tickets, or gaps in coverage as risky, which leads to higher premiums.

Why It Matters

A single speeding ticket or minor accident could increase your premium by 10%–30%. If you have multiple incidents, the rise can be even higher. Insurers reward safe drivers because they’re less likely to file claims.

Expert Advice

From my experience as an auto industry professional, defensive driving courses can help. These courses not only improve your skills but may also qualify you for additional discounts. Check with your insurer to see if they offer any programmes.

Tip: Avoid making small claims if you can afford to pay for minor repairs yourself. This keeps your record clean and prevents premium hikes.

2. Consider Telematics Programmes

Telematics programmes are insurance plans that track your driving behaviour using a smartphone app or a small device installed in your car. Based on how safely you drive, you can earn discounts.

How It Works

These programmes monitor factors like:

- Speeding.

- Braking habits.

- Mileage.

- Time of day you drive.

If you’re a safe and low-mileage driver, you could save 10%–30% or even more.

Examples of Telematics Programmes

- State Farm’s Drive Safe & Save

- USAA’s SafePilot

Personal Note: I’ve seen drivers who saved over £300 annually by joining these programmes. However, if you often drive during rush hours or have aggressive driving habits, it may not work in your favour.

3. Bundle Your Insurance Policies

Bundling means combining multiple insurance policies—like car and home insurance—with the same company. Insurers offer discounts to encourage this.

Benefits of Bundling

- Lower premiums (typically 10%–25%).

- Convenience of managing one account.

- Fewer administrative fees.

Pro Tip: Always compare standalone policies to ensure the bundle actually saves you money. Sometimes, separate providers offer better deals.

4. Adjust Your Coverage Limits

If you drive an older car, consider reducing coverage types like collision or comprehensive insurance. These cover repairs or replacements, but for older vehicles, the cost might outweigh the benefit.

When to Adjust

- If your car’s value is less than £2,000.

- If you have enough savings to cover repairs yourself.

Caution: Never lower your liability coverage below the legal minimum. This could lead to hefty fines or financial trouble after an accident.

5. Pay Annually Instead of Monthly

Paying your premium in full can save you money. Insurers often charge extra fees for monthly payment plans.

Savings Breakdown

- Paying annually can save you up to 10%.

- Avoids monthly administrative costs.

Expert Tip: If paying upfront is challenging, set up a savings plan throughout the year. By the renewal date, you’ll have enough to pay in full.

6. Keep Your Credit Score in Check

In many places, insurers use credit scores to calculate rates. A higher score can mean lower premiums.

How to Improve Your Score

- Pay bills on time.

- Keep your credit utilisation below 30%.

- Avoid opening too many new accounts.

Why It Works

Drivers with good credit are seen as more responsible and less likely to file claims, making them eligible for lower rates.

Telematics Savings Chart

Below is a simple graph showing potential savings through telematics programmes.

| Driving Behaviour | Potential Discount |

|---|---|

| Safe braking and acceleration | 10% |

| Low mileage (under 10,000 miles/year) | 15% |

| Driving during safe hours | 5% |

Final Thoughts

Long-term savings require planning and consistency. Start by driving safely, exploring telematics, and paying attention to details like coverage limits and payment plans. Small changes today can lead to significant savings tomorrow.

For more tips, check out our guide on how to compare auto insurance quotes. It’s a step-by-step breakdown to help you get the best deal.

Here is an image of a telematics device installed in a car. It shows the device plugged into the OBD-II port under the dashboard. The modern car interior highlights the positioning of the device clearly.

By focusing on these strategies, you can lower your car insurance costs while staying protected.

FAQs for New Drivers

Driving for the first time is both exciting and a bit overwhelming. For young drivers and their families, understanding car insurance can feel confusing. Below are clear, simple answers to common questions new drivers often ask.

Does a Teenager With a Learner’s Permit Need Insurance?

Yes, teenagers with learner’s permits typically need insurance. However, there’s good news: most of the time, they’re covered under their parent’s policy.

When a young driver gets a learner’s permit, they don’t need to purchase a separate policy. Parents can simply inform their insurance company about the new driver in the household. Here’s why this works:

- The parent’s policy already covers the car, and the teenager is listed as a permitted driver.

- Coverage ensures the learner is protected in case of an accident, while parents don’t have to start a new policy just yet.

Expert Tip: Let your insurer know as soon as your teen gets a learner’s permit. This avoids complications if a claim is needed later.

Can a Young Driver Get Car Insurance on Their Own?

Yes, but it’s not always the easiest or cheapest option. Here’s what young drivers need to know:

- Eligibility: Young drivers, especially those under 18, often need a parent or guardian to co-sign their policy. This is because minors can’t legally sign contracts.

- Cost Differences: Car insurance for a first-time driver can be expensive. Insurers view new drivers as high-risk due to a lack of driving experience.

- Requirements: To get their own insurance, the driver will need:

- A valid driver’s licence (not just a permit).

- Proof of car ownership if the policy is for their own vehicle.

- Payment history or credit information (which can affect premiums).

Real-Life Insight: When I was a dealership salesperson, I noticed that many young drivers opted to stay under their parents’ policies until they built some driving history. This often saved families hundreds of pounds each year.

Why Is First-Time Car Insurance So Expensive?

First-time car insurance is costly because new drivers are considered higher risks. Here’s why:

- Inexperience: Without a track record of safe driving, insurers rely on statistics. These show that young drivers are more likely to cause accidents.

- Higher Accident Rates: Younger drivers, especially teenagers, tend to have a higher rate of speeding or distracted driving incidents.

Insurance companies balance this risk by charging higher premiums to cover potential claims.

Did You Know? According to UK statistics, drivers aged 17–24 are involved in 15% of serious crashes, despite only making up 7% of all drivers.

Helpful Tips for New Drivers

To make insurance more affordable, here are a few tips for young drivers and their families:

- Choose a Safe Car: Opt for vehicles with high safety ratings and low insurance group ratings.

- Complete a Defensive Driving Course: Some insurers offer discounts to drivers who pass these courses.

- Add an Experienced Driver: Having a parent as a named driver on the policy can reduce costs.

Average Cost of First-Time Insurance (UK)

Average Insurance Costs for Young Drivers (UK)

| Age | Average Premium (£) |

|---|---|

| 17 | 1,900 |

| 18 | 1,700 |

| 19 | 1,400 |

*Data from UK insurance reports, 2023*

Final Thoughts

Starting your driving journey comes with a lot to learn, but getting the right insurance doesn’t have to be stressful. Whether you’re on a parent’s policy or starting your own, make sure you understand what’s covered. It can save both time and money in the long run.

For more detailed advice on auto insurance, check out our complete guide.

Have more questions? Leave them in the comments below!

How to Find Affordable Car Insurance: A Comprehensive Guide

Car insurance can be expensive, but finding affordable coverage is possible. With some effort, research, and smart decisions, you can save money while still meeting your needs. This article will guide you through the steps to help you secure the best rates.

What Affects Car Insurance Costs?

Before diving into ways to save, it’s crucial to understand what affects insurance premiums. Insurers use several factors to calculate your rates:

- Age and Gender: Younger drivers often pay more due to inexperience.

- Driving Record: Accidents and tickets can increase premiums.

- Vehicle Type: Luxury or high-performance cars cost more to insure.

- Location: Urban areas tend to have higher rates than rural ones.

- Credit Score: In some areas, insurers consider credit scores.

These factors can vary by provider, so it’s essential to shop around.

How to Compare Auto Insurance Quotes

Finding the best deal starts with comparing quotes from multiple providers. Follow these simple steps:

- Gather Information

Collect details about your car, driving history, and personal information. - Use Online Comparison Tools

Websites like MoneySuperMarket allow you to compare quotes quickly. - Read the Fine Print

Look for exclusions, deductibles, and limits. Cheap insurance isn’t always better if it doesn’t cover your needs. - Ask About Discounts

Many insurers offer discounts for safe driving, bundling policies, or installing anti-theft devices. - Review and Decide

Once you’ve gathered all the information, select the policy that offers the best value—not just the lowest price.

Expert Advice: Save Money Without Compromising Coverage

As an expert, I’ve seen drivers overpay simply because they didn’t understand their policies. Here are some tips from my experience:

- Bundle Policies: Combine your car and home insurance to get a discount.

- Opt for Higher Deductibles: A higher deductible lowers your premium but means you’ll pay more out of pocket for claims.

- Maintain a Clean Record: Avoid tickets and accidents. This is one of the simplest ways to keep premiums low.

- Drive a Sensible Car: A reliable car with good safety ratings often costs less to insure.

I recall a customer who switched from a luxury sedan to a mid-sized car and saved £500 annually on insurance. Small choices can lead to big savings.

Factors and Their Impact on Insurance Costs

| Factor | Impact on Cost |

|---|---|

| Age | Higher for younger drivers |

| Vehicle Type | Luxury cars cost more |

| Driving Record | Accidents increase premiums |

| Location | Urban areas have higher rates |

Common Mistakes to Avoid

Avoid these pitfalls to ensure you don’t overpay:

- Skipping Comparison: Always compare quotes; loyalty doesn’t always save money.

- Underinsuring: Cheap coverage might leave you paying more in the long run.

- Overlooking Discounts: Ask your provider about every possible discount.

Conclusion

Finding affordable car insurance requires research, comparison, and smart decisions. Take the time to understand your needs and evaluate policies carefully.

Maintain a clean driving record, explore discounts, and don’t be afraid to negotiate with insurers. In the long term, these habits can lead to significant savings while keeping you covered.